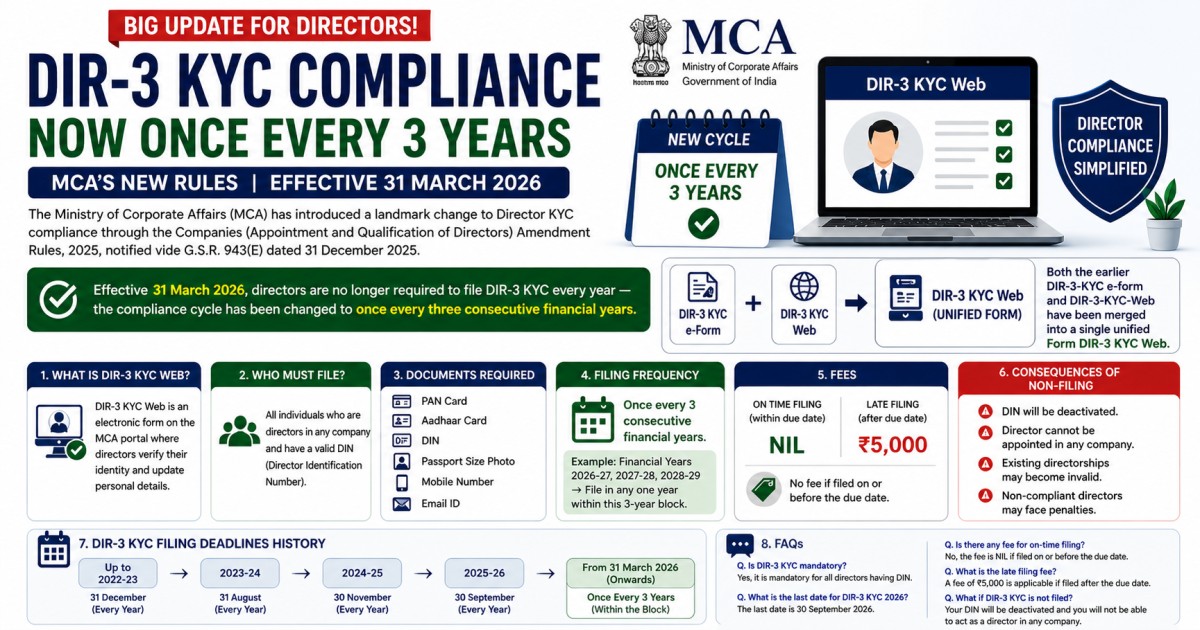

The Ministry of Corporate Affairs (MCA) has introduced a landmark change to Director KYC compliance through the Companies (Appointment and Qualification of Directors) Amendment Rules, 2025, notified vide G.S.R. 943(E) dated 31 December 2025. Effective 31 March 2026, directors are no longer required to file DIR-3 KYC every year — the compliance cycle has been changed to once every three consecutive financial years

⚖️ Important Clarification: Filing is required on or before 30 June of the year immediately following every third consecutive financial year (as per Rule 12A).

. Additionally, both the earlier DIR-3-KYC e-form and DIR-3-KYC-Web have been merged into a single unified Form DIR-3 KYC Web.💡 Why Has MCA Changed DIR-3 KYC?

The earlier annual KYC requirement created repetitive compliance burden for directors with no changes in their personal details. The triennial cycle significantly reduces compliance load while maintaining governance integrity. MCA has simultaneously merged the two existing forms into one unified web form for ease of filing.

🆔 Section 1 — What is Form DIR-3 KYC Web?

Form DIR-3 KYC Web is the web-based KYC compliance form filed by individuals holding a Director Identification Number (DIN) with the Ministry of Corporate Affairs. It confirms and updates a director's KYC particulars — including PAN, mobile number, email address, and residential address — with the Central Government.

Effective 31 March 2026, this single unified form replaces both the earlier DIR-3-KYC (e-form) and DIR-3-KYC-Web (web service). Any pending forms in 'Draft' or 'Pending for DSC upload and payment' status as on 31 March 2026 have been automatically cancelled — directors must file a fresh form.

The form can be filed for the following purposes:

- KYC Compliance — Periodic triennial intimation (every 3 financial years)

- Reactivation of DIN — To reactivate a deactivated DIN with late fee

- Update of Mobile Number — Within 30 days of change

- Update of Email ID — Within 30 days of change

- Update of Permanent Residential Address — Within 30 days of change

- Update of Present Residential Address — Within 30 days of change

👥 Section 2 — Who Must File DIR-3 KYC Web?

The filing obligation applies to every individual who holds a DIN as on 31st March of a financial year — regardless of whether they are currently serving as an active director in any company. This includes:

- All active directors of companies (public, private, OPC, Section 8)

- Directors who have resigned but still hold a valid DIN

- Designated Partners of LLPs holding a DIN/DPIN

- Independent Directors

- Foreign nationals holding a DIN

- Any individual allotted a DIN even if not currently serving on any board

⚠️ Important Note

Merely holding a DIN — even without an active directorship — creates the obligation to file DIR-3 KYC every third financial year. There is no exemption for dormant or resigned directors who retain their DIN.

📜 Section 3 — The 2025 Amendment: What Has Changed?

The Companies (Appointment and Qualification of Directors) Amendment Rules, 2025 (G.S.R. 943(E), 31 December 2025) came into force on 31 March 2026. Here is a complete comparison of what changed:

🔄 Section 4 — Understanding the New 3-Year Filing Cycle

The new triennial KYC system works on a rolling 3-consecutive-financial-year cycle anchored to the financial year in which the DIN was allotted (or the last KYC-compliant financial year). Key mechanics:

- The cycle starts from the financial year in which the DIN was allotted — not from the date of last filing.

- KYC compliance is due by 30 June of the year immediately following every third consecutive financial year.

- If there is no change in KYC particulars, no filing is required for the two intermediate financial years.

- An update filing (for change in mobile/email/address) during the cycle does NOT reset the compliance cycle.

- A DIN holder must hold the DIN as on 31st March of the relevant financial year to be obligated.

⏰ First Major Triennial Deadline

30 June 2028

For directors who last filed DIR-3 KYC for FY 2025-26 (DIN allotted on or before 31 March 2025)

📋 Section 5 — Official MCA Illustrations (3 Scenarios)

The MCA has provided three official illustrations in the advisory to clarify how the 3-year cycle works in practice:

ILLUSTRATION 1

DIN allotted during FY 2025-26

Where a DIN is allotted during FY 2025-26, Form DIR-3 KYC Web shall be filed once every three consecutive financial years. The first filing shall be due from April 2029 to June 2029, and thereafter every third financial year.

📅 First due: April – June 2029

ILLUSTRATION 2

Director already filed KYC for FY 2025-26 (DIN on or before 31 March 2025)

Where a Director already filed DIR-3 KYC (e-form or web) for FY 2025-26, no filing is required for FY 2026-27 and FY 2027-28, provided there is no change in KYC particulars. First filing under the new triennial cycle shall be due from April 2028 to June 2028.

📅 First due: April – June 2028

ILLUSTRATION 3

Update filed mid-cycle (FY 2027-28) — cycle does NOT reset

Where a DIN is allotted on 1 January 2026 (FY 2025-26) and the Director updates mobile number, email ID, or address in FY 2027-28 by filing DIR-3 KYC Web — the 3-year compliance cycle is still reckoned from FY 2025-26 (DIN allotment year). The update in FY 2027-28 does NOT impact the cycle. Next KYC compliance filing remains due April–June 2029.

⚠️ Mid-cycle update does NOT reset the 3-year cycle

Summary: Who Files When?

📎 Section 6 — Documents Required

Mandatory Information / Fields in the Form

- Director Identification Number (DIN)

- Full Name (first, middle, last — no abbreviations)

- Nationality

- Date of Birth (DD/MM/YYYY)

- Income Tax PAN — verified against the IT database

- Passport Number (for foreign nationals)

- Personal Mobile Number — verified via OTP

- Personal Email ID — verified via OTP

- Permanent Residential Address (with country, pin code, district, state/UT)

- Present Residential Address (if different from permanent address)

Attachments Required

Who Certifies the Form?

The requirement of digital signature and professional certification depends on the purpose of filing:

- For periodic KYC (no change in details): No digital signature or professional certification is required. Verification is completed through OTP.

- For update of details or DIN reactivation: The form must be digitally signed by the DIN holder and certified by a practising professional (CA/CS/CMA).

🖥️ Section 7 — Step-by-Step Filing Process on MCA Portal

Here is the complete step-by-step process to file Form DIR-3 KYC Web on the MCA portal (mca.gov.in):

- Login to MCA Portal — Visit mca.gov.in and log in with your MCA registered credentials. First-time users must register using their DIN.

- Navigate to DIR-3 KYC Web — Go to MCA Services → e-Filing → Company/LLP Forms → Director Forms → Select Form DIR-3 KYC Web.

- Select Purpose — Choose one: KYC Compliance, Reactivation of DIN, Update of Mobile Number, Update of Email ID, Update of Permanent Address, or Update of Present Address.

- Enter DIN and Name — Enter your DIN and full legal name. The system auto-populates details from MCA records.

- Verify Existing Mobile and Email via OTP — Enter your registered mobile number and email ID. Verify both using the OTPs received. This step is mandatory for all purposes.

- Fill Personal Details — Complete full name (first/middle/last), nationality, date of birth, Income Tax PAN (auto-verified against IT database), and passport number (for foreign nationals).

- Enter Updated Details (if applicable) — If filing for an update, enter the new mobile/email/address details and verify via OTP. Enter full permanent and present residential addresses.

- Upload Attachments — Attach proof of change in particulars (if updating), select residential proof document type from the dropdown. Max file size: 2 MB per attachment.

- DIN Holder's Digital Signature — Required only in case of update of details or DIN reactivation. Not required for normal KYC.

- Professional Certification — Required only where there is a change in particulars or for DIN reactivation.

- Submit and Pay — Click Submit. For periodic KYC filed on time (by 30 June), fee is NIL. For late filing or updates, prescribed fee applies via the MCA payment gateway.

- Download SRN Acknowledgement — After successful submission, download the Service Request Number (SRN) receipt as proof of filing.

✅ Pro Tip Before You Start

Keep your personal mobile number and email ID accessible — OTPs will be sent to both, and they expire quickly. Also ensure your DSC is valid and registered on the MCA portal before starting. For update filings, have your supporting document (Aadhaar/Utility Bill etc.) scanned and ready in PDF/JPG under 2 MB.

💰 Section 8 — Fee Structure

✅ On-Time Filing

NIL

Filed on or before 30 June of the due year (every 3rd FY)

❌ Late Filing / Reactivation

₹5,000

Filed after 30 June, or for DIN reactivation

⚠️ Section 9 — Consequences of Non-Filing / DIN Deactivation

Failure to file DIR-3 KYC Web by the prescribed deadline triggers serious legal and operational consequences:

🚨 Ripple Effect on Companies

If a director of a small private company (particularly one with only 2 directors) fails to file DIR-3 KYC and their DIN gets deactivated, the company may be unable to submit its annual return, financial statements, or any other MCA form requiring that director's DIN or DSC — triggering further late fees and penalties for the company itself.

📅 Section 10 — DIR-3 KYC Filing Deadline History

The complete chronological history of DIR-3 KYC compliance deadlines and changes since the form was first introduced in 2018: