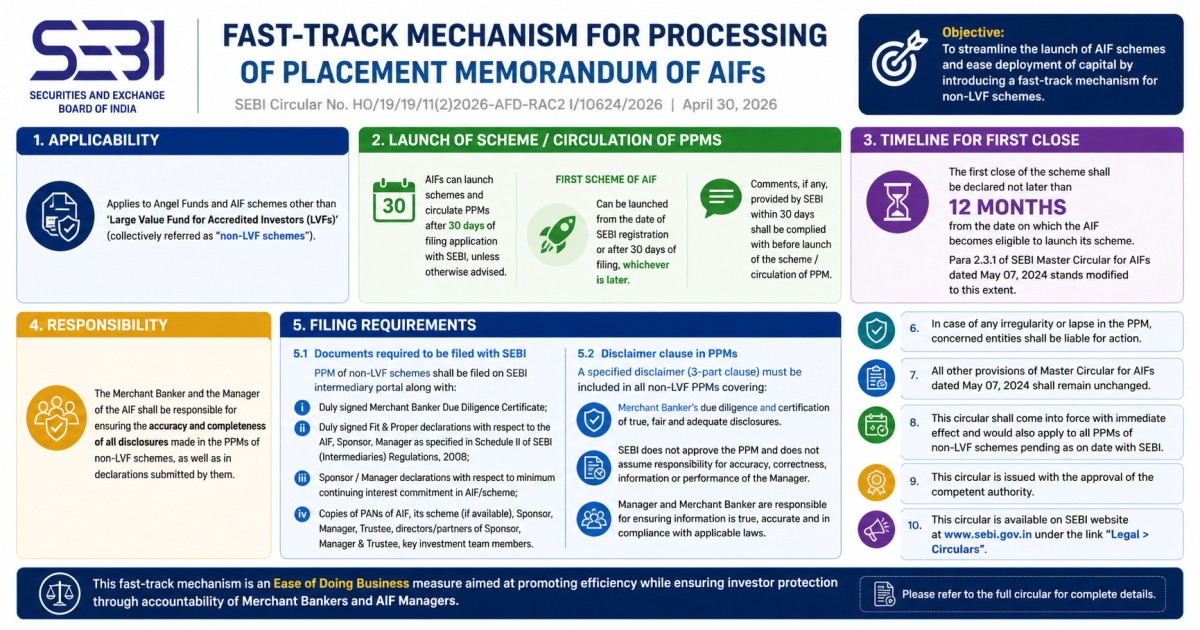

The Securities and Exchange Board of India (SEBI) has introduced a significant Ease of Doing Business reform for Alternative Investment Funds (AIFs) vide Circular No. HO/19/19/11(2)2026-AFD-RAC2 I/10624/2026 dated April 30, 2026. The circular establishes a Fast-Track Mechanism for Processing of Private Placement Memoranda (PPMs) of non-LVF AIF schemes, allowing AIFs to launch their schemes and circulate PPMs to investors after just 30 days of filing with SEBI — without waiting for SEBI's formal comments or approval. This circular has immediate effect and also applies to all PPMs of non-LVF schemes pending with SEBI as on April 30, 2026.

💡 Why Has SEBI Introduced This Fast-Track Mechanism?

Under the earlier procedure, SEBI reviewed PPM disclosures, merchant banker due diligence certificates and related documents before allowing an AIF to launch its scheme — a process that was time-consuming and delayed capital deployment. This fast-track mechanism removes that pre-launch review bottleneck for non-LVF schemes, shifting accountability squarely onto Merchant Bankers and AIF Managers.

📌 Section 1 — What is the Fast-Track Mechanism?

The fast-track mechanism is a streamlined PPM processing system introduced by SEBI for non-LVF AIF schemes (which includes Angel Funds and all AIF schemes other than Large Value Funds for accredited investors). Under this mechanism:

- AIFs can launch new schemes and circulate PPMs to investors for soliciting funds after 30 days of filing the application with SEBI — without waiting for SEBI's review to conclude.

- SEBI's prior written approval or formal clearance is no longer required before launch of non-LVF schemes.

- Responsibility for accuracy and completeness of all PPM disclosures shifts to the Merchant Banker and the AIF Manager.

- SEBI may still provide comments during the 30-day window — and these must be complied with before launch.

🏦 Section 2 — Which AIFs Are Covered? (Non-LVF Schemes)

The fast-track mechanism applies to "non-LVF schemes" — defined in the circular as:

💡 What is an LVF?

A Large Value Fund (LVF) for Accredited Investors is an AIF scheme where each investor commits a minimum investment of ₹70 crore and all investors are SEBI-accredited investors. LVFs continue to follow the earlier, more stringent SEBI review process and are not covered by this fast-track circular.

⏱️ Section 3 — Launch Timeline: The 30-Day Rule

The circular prescribes a clear two-scenario framework for determining when a non-LVF AIF scheme can be launched:

SCENARIO A — Existing AIF, New Scheme

Para 4.1.1 — Standard Fast-Track Rule

In terms of Regulation 12 and 19 of SEBI (AIF) Regulations, 2012, AIFs can proceed with the launch of their new schemes and circulate the PPM to investors for soliciting funds after 30 days of filing of application with SEBI, unless otherwise advised by SEBI during that period.

📅 Eligible to launch: Day 31 from filing date (or earlier if SEBI confirms no comments)

SCENARIO B — First Scheme of a Newly Registered AIF

Para 4.1.2 — "Whichever is Later" Rule

For the first scheme of an AIF, the AIF can proceed with launch from:

(a) the date of grant of SEBI registration, OR

(b) after 30 days of filing of application with SEBI, whichever is later.

⚠️ Both conditions must be met — registration must be granted AND 30-day filing period must elapse

⚠️ Para 4.1.3 — SEBI Comments Must Be Complied With Before Launch

If SEBI provides any comments during the 30-day window, the Merchant Banker and AIF must comply with all such comments before launching the scheme or circulating the PPM. The fast-track mechanism does not override SEBI's right to raise issues — it only removes the requirement to await SEBI's formal written clearance before launch.

📅 Section 4 — Timeline for First Close

Para 4.2 of the circular prescribes a mandatory deadline for the first close of non-LVF schemes:

⏰ Mandatory First Close Deadline

Within 12 months

from the date on which the AIF becomes eligible to launch its scheme under Para 4.1.1 or 4.1.2

This provision modifies Para 2.3.1 of the SEBI Master Circular for AIFs dated May 07, 2024 to this extent. All other provisions of that Master Circular remain unchanged.

📋 Section 5 — Filing Requirements with SEBI

PPMs of non-LVF schemes must be filed on the SEBI Intermediary Portal along with the following documents, in addition to payment of the applicable scheme fee:

📝 Section 6 — Mandatory Disclaimer in PPMs

Para 5.2 of the circular mandates that all non-LVF scheme PPMs must include the following disclaimer clause. This disclaimer is legally significant as it clearly delineates SEBI's non-approval role and Merchant Banker/Manager responsibility:

"1. Merchant Banker viz., [Name of Merchant Banker] has independently exercised due-diligence regarding the information given in the placement memorandum, including the veracity and adequacy of disclosures made therein. Merchant Banker has certified in its Due-Diligence Certificate dated ______ submitted to SEBI that the disclosures made in the placement memorandum are true, fair and adequate to enable the investors to make an informed decision with respect to the investment in the proposed Scheme/Fund and such disclosures are in accordance with the requirements of Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012, circulars, guidelines issued thereunder and other applicable legal requirements.

2. It is to be distinctly understood that submission of the PPM to SEBI should not in any way be deemed or construed that the same has been approved by SEBI. SEBI does not assume any responsibility for the accuracy and correctness of disclosures, facts and claims made in the PPM and for the capability and performance of the Manager.

3. The Manager and Merchant Banker are responsible for ensuring that the information contained in the PPM is true and accurate in all material respects and in compliance with SEBI (Alternative Investment Funds) Regulations, 2012 and other applicable laws and that there are no material facts, the omission of which would make any statement in this memorandum, whether of fact or opinion, misleading."

⚖️ Section 7 — Responsibility Framework & Accountability

The fast-track mechanism shifts the compliance responsibility framework significantly. Here is a clear breakdown of who is responsible for what:

🚨 Penal Consequences for Lapses

Para 6 of the circular is unambiguous: "In case of any irregularity or lapse in the PPM, concerned entities shall be liable for action." This means both the Merchant Banker and the AIF Manager face regulatory action by SEBI for any deficiencies, misrepresentations, or omissions in the PPM — since SEBI's pre-approval process has been removed.

🔄 Section 8 — What Has Changed vs. Earlier Process?

🗓️ Section 9 — Key Dates & Regulatory References

❓ Section 10 — Frequently Asked Questions

📝 Bottom Line — What This Means for AIFs and Merchant Bankers

SEBI's fast-track mechanism is a genuine ease-of-doing-business reform that significantly reduces the time-to-market for non-LVF AIF schemes. AIFs can now begin soliciting capital from investors within 30 days of PPM filing — instead of waiting months for SEBI's formal comments and revised PPM acceptance.

However, this faster launch comes with a clear trade-off: the entire burden of disclosure accuracy, legal compliance, and investor protection now rests squarely with the Merchant Banker and AIF Manager. Any irregularity or omission in the PPM will directly attract regulatory action — with SEBI explicitly disclaiming responsibility for PPM accuracy.

Merchant Bankers must significantly strengthen their due diligence processes. AIF Managers must ensure all PPM disclosures are complete, accurate, and legally compliant before filing — since the 30-day launch window begins from the date of filing itself.

Source: SEBI Circular No. HO/19/19/11(2)2026-AFD-RAC2 I/10624/2026 dated April 30, 2026 — Fast-Track Mechanism for Processing of Placement Memorandum of AIFs filed with SEBI. Available on sebi.gov.in under Legal Framework – Circulars and Info for – Alternative Investment Funds. For more regulatory updates, visit corplawupdates.in. This article is for informational purposes only and does not constitute legal or investment advice.