📌 Key Facts at a Glance

No. 02/2026

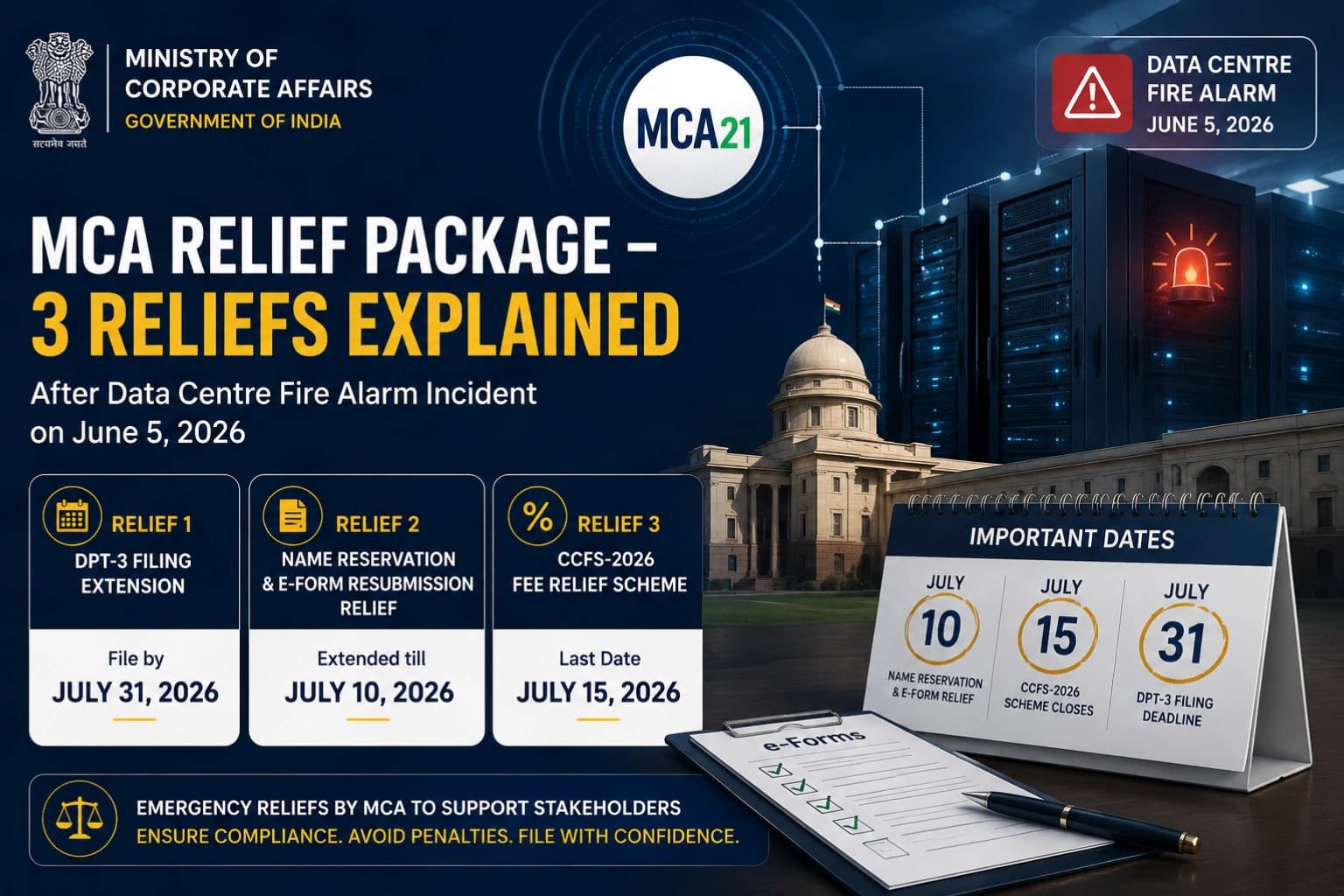

The Ministry of Corporate Affairs has extended the due date for filing Form DPT-3 for FY 2025–26 from 30 June 2026 to 31 July 2026, without payment of additional fees. The extension has been granted in view of capacity disruption at the MCA Data Center following a fire incident on 05 June 2026.

The Ministry of Corporate Affairs (MCA) has issued General Circular No. 02/2026 dated June 19, 2026, bearing F.No. Policy-02/2/2020-CL-V-MCA, extending the due date for filing Form DPT-3 (Return of Deposits) for the financial year ended 31 March 2026. The circular, signed by Indrajit Vania, Joint Director (Policy), is addressed to DGCOA, all Registrars of Companies, all Regional Directors, and all Stakeholders.

Companies that were required to file Form DPT-3 for FY 2025–26 by 30 June 2026 will now be able to do so without incurring additional fees up to 31 July 2026. The extension has been issued with the approval of the competent authority and is in direct response to the disruption caused by a fire incident at the MCA Data Center.

📜 Background — Why Was the Extension Granted?

Form DPT-3 is an annual return that companies are required to file under the Companies Act, 2013 read with the Companies (Acceptance of Deposits) Rules, 2014. For FY 2025–26, the standard due date for filing this return was 30 June 2026 (i.e., within 90 days from the close of the financial year ended 31 March 2026).

📋 What Is Form DPT-3 and Who Must File It?

Form DPT-3 is a Return of Deposits required to be filed annually under Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014 read with Section 73 of the Companies Act, 2013. It serves two distinct disclosure purposes — and accordingly, there are two categories of companies that must file it:

⚙️ What the Circular Says — The Operative Provision

📋 Before vs. After — DPT-3 Filing Timeline for FY 2025–26

📊 Impact Analysis — Who Benefits

🏢 All Companies with Outstanding Deposits / Receipts

Every company that was required to file DPT-3 for FY 2025–26 now has until 31 July 2026 without incurring additional fees. This covers companies with outstanding actual deposits, exempted deposits, inter-corporate loans, director loans, and other outstanding receipts as on 31 March 2026.

📋 CS / CA Professionals & Compliance Teams

Company Secretaries and Chartered Accountants advising multiple companies on MCA filings now have a full additional month to complete, verify, and file DPT-3 returns for their clients — without the pressure of additional fee liability from 1 July 2026 onwards.

🖥️ MCA Portal Users

The extension also provides buffer time for MCA to complete its data center restoration activities, reducing the likelihood of last-minute portal congestion that often occurs when many companies file simultaneously close to a deadline.

✅ Compliance Action Points

- ✅ File DPT-3 on or before 31 July 2026 to avoid additional fees. The extension covers only the period up to 31 July 2026 — filings after this date will attract additional fees as per the Companies (Registration Offices and Fees) Rules, 2014.

- ✅ Do not wait until 31 July 2026: Last-minute filings on or around the extended deadline risk portal congestion on MCA21. Prepare all DPT-3 data — outstanding deposits, exempted deposits, inter-corporate loans, director loans, and other receipts as on 31 March 2026 — and file well in advance of the deadline.

- ✅ Check applicability carefully: DPT-3 filing is required even by companies that have not accepted any "deposits" in the technical sense — if there are outstanding amounts received that are exempt from the definition of deposits (e.g., unsecured loans from directors, inter-corporate borrowings), these must be disclosed. Companies that genuinely have no outstanding amounts of any kind under DPT-3 scope should confirm this position on record.

- ✅ CS/CA professionals advising multiple clients: Update your compliance calendar for all clients — replace the 30 June 2026 DPT-3 deadline with 31 July 2026. Inform clients that the extension is automatic (no separate application needed) and is granted in view of the MCA Data Center fire incident.

The circular grants relief only from additional fees for late filing — it does not alter the substantive compliance obligations under the Companies (Acceptance of Deposits) Rules, 2014. The return still covers the period ending 31 March 2026, and all outstanding amounts as on that date must be reported accurately. The extension does not affect any other MCA filing deadlines for FY 2025–26.

Looking for a detailed guide on how to file DPT-3 — including late fees, documents required, who must file, and step-by-step MCA21 filing instructions? We have a comprehensive guide covering everything.

This article is for informational purposes only and does not constitute legal advice. Verify all details against the official MCA circular before relying on this content for compliance purposes.