The Insolvency and Bankruptcy Board of India (IBBI) has notified significant amendments to the IBBI (Insolvency Resolution Process for Personal Guarantors to Corporate Debtors) Regulations, 2019 vide Notification No. IBBI/2026-27/GN/REG149 dated 01 June 2026, effective 02 June 2026. These are among the most substantive changes to the personal guarantor insolvency framework since the regulations came into force on December 01, 2019. The amendment introduces a landmark mandatory asset disclosure framework (new Regulation 6A), mandates coordination between resolution professionals of personal guarantors and corporate debtors (new Regulation 11A), streamlines the repayment plan meeting process (new Regulation 17A), tightens the non-submission of repayment plan procedure (amended Regulation 17B), replaces form-based references with circular-based formats, and removes the three prescribed forms from the regulation itself. This guide covers every chapter, every regulation, every amendment — with current vs proposed comparisons, practical impact, and FAQs.

⚡ Notification at a Glance

GN/REG149

(w.e.f. 02-06-2026)

23 Regulations

Reworked

Removed

As of mid-2025, 664 cases had been admitted for insolvency resolution of personal guarantors — yet 143 had been closed on account of non-submission or rejection of repayment plans. This exposed a critical procedural gap: what happens when no repayment plan is prepared after admission? The June 2026 amendments directly address this gap while simultaneously introducing sweeping transparency requirements (mandatory asset disclosure including crypto, ESOPs, overseas investments) and inter-process coordination mechanisms with corporate debtor insolvency proceedings.

👤 Who Do These Regulations Apply To?

The IBBI (Insolvency Resolution Process for Personal Guarantors to Corporate Debtors) Regulations, 2019 apply only where:

- the debtor is an individual personal guarantor to a corporate debtor (company or LLP), and

- the guarantee in favour of a creditor has been invoked and remains unpaid in full or in part, and

- an application under Sections 94 or 95 of the Insolvency and Bankruptcy Code, 2016 is filed before the NCLT as the adjudicating authority.

They do not govern fresh‑start processes or ordinary individual/partnership insolvencies before the Debt Recovery Tribunal; those remain under the general Part III framework and separate rules.

📜 Section 1 — Amendment History: How the Regulations Have Evolved

📘 CHAPTER I — PRELIMINARY (Regulations 1–3)

Regulation 1 — Short Title & Commencement

These regulations are called the IBBI (Insolvency Resolution Process for Personal Guarantors to Corporate Debtors) Regulations, 2019. They came into force on December 01, 2019 — the same date on which Part III of the IBC (governing insolvency of individuals and partnerships) was brought into force for personal guarantors to corporate debtors. Unchanged by the June 2026 amendment.

Regulation 2 — Application

These regulations apply exclusively to the insolvency resolution process for personal guarantors to corporate debtors — i.e., individuals who have given personal guarantees on behalf of companies undergoing or susceptible to insolvency. They do not apply to fresh-start processes or bankruptcy of other individuals. Unchanged by the June 2026 amendment.

Regulation 3 — Definitions 🔴 AMENDED

📗 CHAPTER II — GENERAL (Regulations 4–6A)

Regulation 4 — Eligibility of Resolution Professional 🔴 AMENDED

An insolvency professional (IP) is eligible as resolution professional (RP) only if three conditions are met:

The January 2024 amendment (REG107) removed the earlier restriction that prevented an IP who had acted as interim resolution professional, resolution professional, or liquidator in respect of the corporate debtor from being appointed as RP for the personal guarantor. This change — already in the consolidated regulations — recognises that such an IP may in fact be best positioned to handle the guarantor's resolution given their knowledge of the corporate debtor's affairs.

Regulation 5 — Preservation of Records

The resolution professional must preserve both a physical and electronic copy of all records relating to the guarantor's resolution process, in accordance with the record retention schedule as communicated by IBBI in consultation with insolvency professional agencies. This is a continuing obligation throughout the process and beyond. Unchanged by the June 2026 amendment.

Regulation 6 — Debt Counselling

Debt counselling may be provided to a guarantor by such person as may be recognised by IBBI or the Central Government. This is an enabling provision — it allows debt counselling but does not make it mandatory or define a standard format. Unchanged by the June 2026 amendment.

🆕 Regulation 6A — Statement of Assets NEW — Inserted w.e.f. June 02, 2026

This is the most significant insertion in the June 2026 amendment. Regulation 6A requires that along with an application for initiating insolvency resolution process (whether under Section 94 by the guarantor, or Section 95 by a creditor), a complete and true statement of ALL assets with supporting evidence must be filed with the Adjudicating Authority. The statement is exhaustive — covering 12 categories of assets.

The statement must mandatorily include assets across five dimensions of ownership — no asset can be excluded on the basis of formal legal title:

📙 CHAPTER III — REGISTRATION OF CLAIMS (Regulations 7–10)

Regulation 7 — Submission and Verification of Claim 🔴 AMENDED

Key substantive rules under Regulation 7 (unchanged):

- Creditor bears costs of submitting the claim

- Claims may be proved via information utility records or documentary evidence

- RP can call for additional evidence or clarifications

- RP must verify each claim and prepare list of creditors within 30 days from public notice

- Where claim amount is uncertain — RP makes best estimate based on available information

- Estimates may be modified as additional information comes in — up until approval of the repayment plan

- Claims in foreign currency must be valued in Indian rupees at the RBI official exchange rate on the resolution process commencement date

Regulation 8 — Transfer of Debt Due to Creditors

If a creditor assigns or transfers their debt during the resolution process, both the assigning creditor and the assignee/transferee must provide the RP with the terms of the assignment and the identity and details of the new creditor. The RP must then notify all creditors and the Adjudicating Authority of the change in the creditors list within two days. This ensures real-time maintenance of the creditor register. Unchanged.

Regulation 9 — List of Creditors

The list of creditors under Section 104(1) must contain: names, amount claimed, amount admitted, and security interest (if any) for each creditor. The RP must: (a) make it available for inspection by claim-submitters; (b) serve a copy on the guarantor; (c) make it available on the guarantor's website if any; (d) present it at the meeting of creditors; and (e) file a certified copy with the AA along with the repayment plan. Unchanged.

Regulation 10 — Statement of Affairs

The RP must prepare a comprehensive statement of affairs for the purposes of Section 107(3)(b), covering for the preceding 3 financial years and the current financial year: assets & liabilities, excluded assets & excluded debts, income statements, income-tax returns, creditor-wise amounts (secured/unsecured), debts owed to associates, guarantees given, and financial statements for any business owned. Unchanged.

📕 CHAPTER IV — MEETINGS OF CREDITORS & VOTING (Regulations 11–16)

Regulation 11 — Meeting of Creditors 🔴 AMENDED

🆕 Regulation 11A — Facilitation of Transfer of Assets REPLACED w.e.f. June 02, 2026

The earlier version of Regulation 11A (inserted in January 2024) dealt with meeting-related disclosures of the repayment plan. The June 2026 amendment replaced it entirely with a new, more significant provision governing cross-process asset transfer coordination — one of the most practically important changes in this amendment.

In practice, a promoter who is a personal guarantor may have assets that overlap with (or are affected by) the corporate debtor's resolution plan. Without a coordination mechanism, the RP handling the CIRP and the RP handling the personal guarantor's IRP might take conflicting positions on the same assets. Regulation 11A creates a formal bridge — requiring the guarantor's creditors to consent to any such cross-process transfer, and requiring the RP to disclose it in statutory reports.

Regulation 12 — Contents of Meeting Notice

Meeting notices must inform participants of venue, time, date, and options — (i) to attend in person, via video conferencing, or by proxy; and (ii) for creditors to vote in person, by proxy, by electronic means, or electronic proxy. The notice must carry an agenda including list of matters for discussion, issues for voting, and relevant documents. For video conferencing or e-voting, login credentials, password generation details, and contact details of the facilitator must be included. Unchanged by June 2026 amendment.

Regulation 13 — Quorum

- Quorum: Creditors representing at least 33% of voting share — present in person, by proxy, or via video conferencing

- Creditors may modify this percentage for future meetings at any meeting

- If quorum not achieved: meeting auto-adjourned to same time and place the next day — with no quorum requirement on the adjourned day (unless creditors had decided otherwise)

Regulation 14 — Conduct of Meeting

- RP presides over the meeting

- Roll call at commencement — each participant states name, capacity, creditor represented (if any), and confirmation of receipt of agenda

- RP confirms quorum after roll call and ensures it is maintained throughout

- Only participants and RP-authorised persons may attend — no uninvited observers

Regulation 15 — Voting by Creditors

The voting process has a two-stage structure to ensure maximum creditor participation:

Regulation 16 — Voting by Proxy 🔴 AMENDED

The proxy must not be an associate of the guarantor, and may vote by electronic means. These substantive rules are unchanged.

📒 CHAPTER V — REPAYMENT PLAN (Regulations 17–23)

Regulation 17 — Contents of Repayment Plan

🆕 Regulation 17A — Meeting of Creditors for Repayment Plan Originally Jan 2024; Retained in June 2026

The RP must place the repayment plan (as mentioned under Section 105 of the IBC) before a meeting of creditors for its consideration. Proviso (crucial): Where no repayment plan has been received within the period stipulated under Section 106, the RP must notify this fact in a meeting of creditors — so creditors are actively informed of the non-submission, triggering the Regulation 17B pathway.

📝 Regulation 17B — Non-Submission of Repayment Plan AMENDED — Reference Updated June 2026

IBBI data showed that of 664 admitted personal guarantor IRP cases, 143 had been closed due to non-submission or rejection of repayment plans — creating a vacuum where no resolution or bankruptcy order was being passed. Regulation 17B + amended Section 106(1A) of the IBC now create a formal pathway: if no repayment plan is submitted, the RP (with creditor approval) files a specific application under Section 106(1A) for the AA to pass appropriate orders — which may include converting the proceeding to a bankruptcy order.

Regulation 18 — Purchase of Assets by Certain Persons

The following persons are barred from purchasing or acquiring any interest in the guarantor's property (directly or indirectly) without Adjudicating Authority permission: the RP or any partner/director of his IPE; any professional appointed by the RP for the process; any creditor; any company where the guarantor or a creditor is a promoter or director; and any associate of the guarantor, creditor, or RP. Any purchase made in contravention may be set aside by the AA. Unchanged.

Regulation 19 — Filing with the Adjudicating Authority

- RP must file the creditor-approved repayment plan with the AA along with the report under Section 106 or 112 (as applicable) — within 120 days from the resolution process commencement date

- RP must provide copies of all filed documents to the guarantor and creditors within 3 days of filing with the AA

Regulation 20 — Breach of Repayment Plan by the Guarantor

Regulation 21 — Application for Discharge Order

For the purposes of a discharge order, the RP files an application along with copies of the notice and report under Section 117 to the AA under Section 119. The AA may then pass the discharge order on consideration of these materials. Unchanged.

Regulation 22 — Non-Cooperation by Guarantor

If the guarantor fails to cooperate at any time during the resolution process period or during repayment plan implementation, the RP prepares a statement to this effect and files it with the AA for appropriate directions. Unchanged.

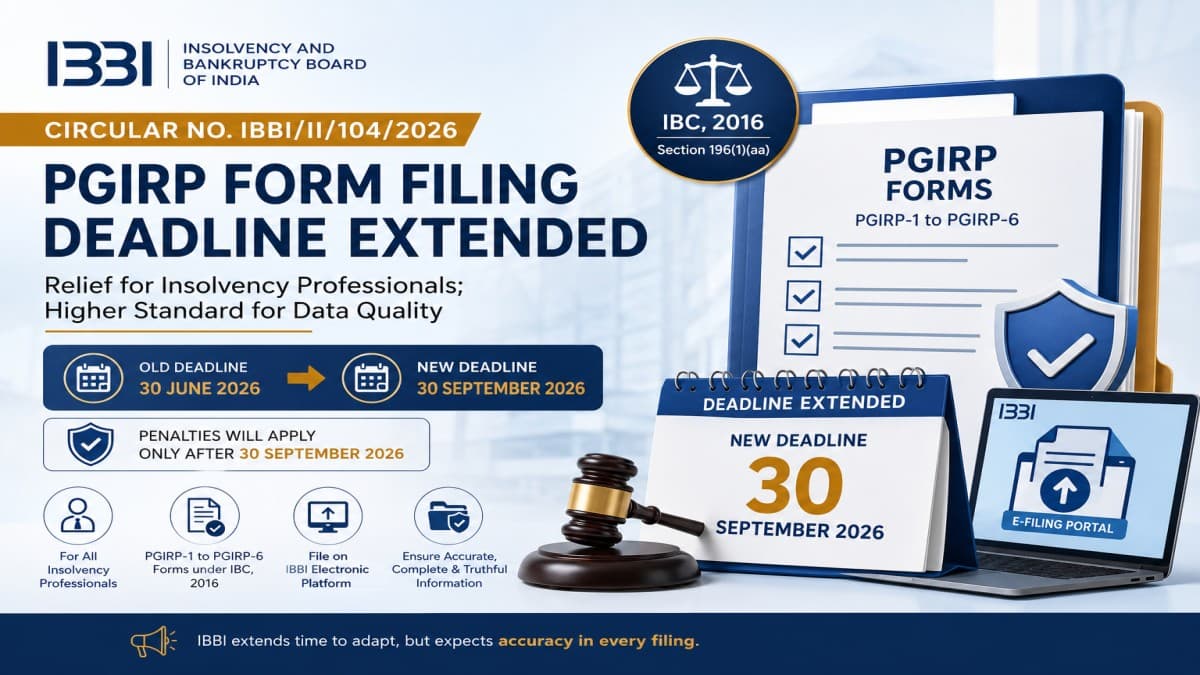

Regulation 23 — Filing of Forms Inserted Nov 2025; Forms Moved to Circular by June 2026

Regulation 23 was inserted in November 2025 and creates a statutory framework for mandatory form filing — with penalties for delay or inaccuracy:

- RP must file Forms with enclosures as notified by IBBI through circular, within stipulated timelines

- IBBI provides Forms on its electronic platform; may modify them from time to time

- RP must ensure Forms and enclosures are accurate and complete

- Late filing fee: ₹500 per Form per calendar month of delay

- Consequences of non-compliance: IBBI may take any action including refusal to issue or renew Authorisation for Assignment (AFA) — the RP's licence to take up cases

📋 Section 7 — Forms A, B & C — From Regulations to Circular

One of the most practically significant structural changes in the June 2026 amendment is the removal of Forms A, B, and C from the body of the regulation and their relocation to a separate IBBI Circular (IBBI/IIRP/98/2026 dated June 02, 2026). This gives IBBI the flexibility to update the forms without amending the regulations each time. Here is what each form covers:

📊 Section 8 — Complete Before vs After: All June 2026 Changes

❓ Section 9 — Frequently Asked Questions

✅ Section 10 — Compliance Action Checklist

- ✅For Personal Guarantors filing applications from June 02, 2026: Prepare a comprehensive Regulation 6A statement of assets covering all 12 categories and 5 dimensions of ownership — with supporting evidence (bank statements, share certificates, crypto wallet screenshots, property documents, income-tax returns)

- ✅Digital asset disclosure: Declare all cryptocurrencies, NFTs, VDAs, and domain names with current market value as of the application date — obtain valuation evidence from licensed exchanges where possible

- ✅ESOP and beneficial ownership: Disclose all ESOPs (vested and unvested), nominee holdings, HUF assets, and trust interests — even if legal title does not rest with the guarantor

- ✅Creditor applications (Section 95): File asset information to the extent available — no obligation to file complete guarantor asset details, but include all information in creditor's possession

- ✅Resolution Professionals — update consent forms: Form A for written consent is no longer appended to the regulations — use the IBBI Circular (IBBI/IIRP/98/2026 dated June 02, 2026) format

- ✅Creditors — update claim forms: Form B is now issued via circular — ensure claims are filed in the updated circular format

- ✅Concurrent CIRP situations (Reg. 11A): If the personal guarantor's IRP runs concurrently with the corporate debtor's CIRP, the RP must actively coordinate on asset transfers under Section 28A — obtain creditor meeting approval before any cross-process transfer and disclose in Section 106/112 reports

- ✅Repayment plan process: If no repayment plan is received in the Section 106 period, notify creditors in a meeting (Reg. 17A proviso) and then file application under Section 106(1A) with creditor approval (Reg. 17B) — do not leave the case in limbo

- ✅Form filing timelines (Reg. 23): File all IBBI-specified Forms within stipulated timelines — late filing attracts ₹500/form/calendar month of delay and may result in AFA non-renewal

- ✅Proxy appointments: Use the Form C issued under Circular IBBI/IIRP/98/2026 — deliver to RP at least 24 hours before the meeting; old forms appended to the regulations are no longer valid

This article is for informational and educational purposes only and does not constitute legal advice. For specific insolvency matters, consult a registered insolvency professional or legal counsel.